Can Muslims invest in a 401(k) plan?

Is it permissible to join a 401(k) plan?

Here, we will summarize the basics of 401(k) plans, and explain the religious duties related to this investment opportunity both ahead of retirement and at the time of retirement.

What is a 401(k)?

A 401(k) is a type of retirement savings plan offered by many employers in the United States, where employees save and invest a portion of their paychecks.

Although the 401(k) retirement plan is exclusive to the United States, other countries offer retirement savings plans with a similar concept, such as Canada’s Registered Retirement Savings Plan (RRSP) or the United Kingdom’s Workplace Pension.

How does a 401(k) plan work?

Here are the basics of how 401(k) plans work:

- Employees determine the percentage of their income they wish to contribute to their 401(k) plan.

- The above amount is automatically withheld from the employee’s paycheck and deposited into their 401(k) account.

- Employers will often provide a matching contribution as an incentive. The employer’s contribution typically matches a certain percentage of the employee’s contribution.

- Both the employee’s and employer’s contributions are then invested in long-term assets designed to grow over time.

- Withdrawals from a 401(k) are generally restricted until retirement.

- Withdrawals made before an employee has reached the eligible age often incur significant fees and penalties.

Here are simple definitions of the three main components of a 401(k) plan.

| Employee contribution | Employer match | Investment return |

| This is the amount deducted from the employee’s salary. | This is the amount that the employer contributes as a benefit or bonus. | This means the profits and returns generated from the amount invested. |

What is our religious obligation regarding 401(k)?

When calculating one’s obligation to pay khums (a form of Islamic tax), the three aforementioned components of the 401 (k) plan must be evaluated individually and then summed at the end. The breakdown is as follows:

- Employee Contribution – This portion is subject to khums immediately*. This portion is a percentage of the employee’s salary that has been set aside for savings, making it a surplus to his annual expenses. Therefore, khums must be paid on it if he can withdraw it or from other money he has on hand, either at each monthly contribution or at the end of his Khums Year. If he is unable to do so and cannot withdraw it, then he should pay khums on it when he can or upon receiving it.

- Employer Match – This portion is subject to khums once it is withdrawn. Once withdrawn, the person has until the end of their khums-year date to spend it on his expenses, and whatever remains is subject to khums.

- Investment Return – This portion is not subject to khums until it is withdrawn. Once withdrawn, this portion may be further divided into two categories, depending on whether the investments are based on religiously legitimate and permissible transactions or prohibited/haram ones:

- Religiously Permissible: The ruling is the same as the Employer Match—meaning, upon receiving the money, the person has until the end of his khums year to spend this money on his expenses, and whatever remains is subject to khums.

- Religiously Impermissible: Half of the investment returns must be given in charity to poor believers, and khums must be paid on the remaining half if it is not spent on personal expenses and the khums year ends.

Demonstrative Example 1:

As a hypothetical example to demonstrate the concept, consider the following scenario:

Beginning on January 1st, an employee enrolls in his company’s 401(k) savings plan. He earns a monthly salary of $5,000 and decides to have 10% of his monthly paycheck ($500) deducted and deposited into his 401(k) account. His employer matches 50% of his contributions each month ($250).

The following demonstrates the transactions rendered every month:

| Employee’s Contribution | Employer Contribution | Investment Return | Khums Due Each Month | |

| Sample Month | $500 | $250 | $35(this amount will grow over time depending on how much has been invested and where the money is being invested) | When the paycheck is received, $100 must be paid in khums* |

Each month, the employee owes $100 in khums upon receiving his paycheck. This can be paid immediately, or at the end of his khums year.

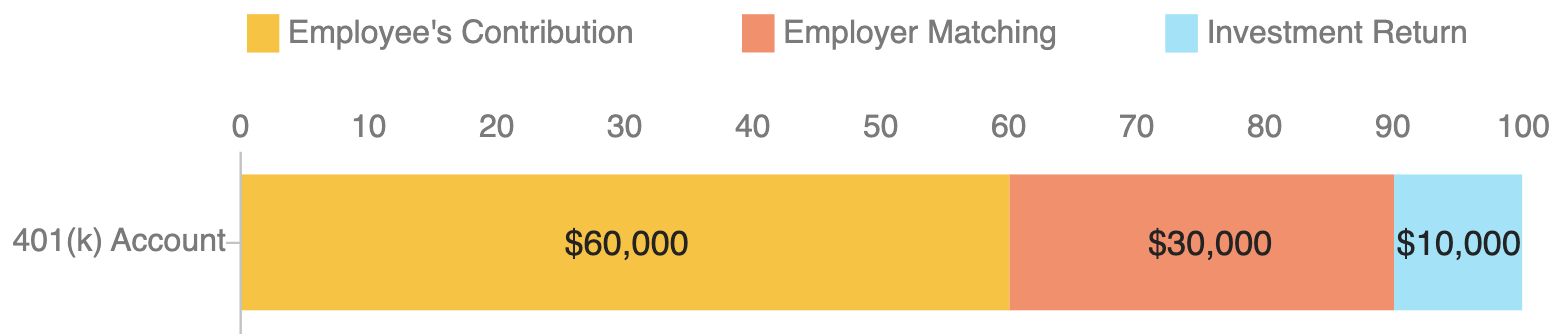

After 10 years of employment, the employee retires and withdraws his 401(k) balance with a total of $100,000, with the following breakdown:

Khums Obligation After 401(k) Withdrawal:

- Employee’s Contribution: Since the employee would pay khums each month, there is no obligation for khums on this portion. The total that would have been paid should be: $100 x 120 months = $12,000

- Employer’s Match: The $30,000 received from the employer’s match is khums-applicable—meaning, if any of this portion remains at the end of the khums year, khums must be paid.

- Investment Return: The $10,000 generated from the returns from investment is treated like the employer’s match portion unless the investments were generated from impermissible sources. If so, then $5,000 must be paid as charity to the poor believers, and khums is owed on what remains from the other half at the end of the khums year after spending on one’s expenses.

*Note: Anytime a person is subject to paying khums immediately (before their end-of-year due date), as in the case of paying khums on the monthly amount deducted from the employee’s paycheck for 401(k) contributions, one must consider whether or not the money being used to pay that immediate khums payment has been paid khums on or not. So, if you are using money from your current year’s earnings, which has not been paid khums on yet, then you must pay 25% instead of 20%. Otherwise, if you are using money from a previous year’s earnings and you have already paid khums on it, then the regular approach of paying khums (20%) is due.

Non-Employer-Based Retirement Saving Plans

The 401(k) retirement savings and other similar plans in other countries are offered through employers. However, retirement saving plans are also offered at financial institutions such as banks where one can individually enroll in, known as Individual Retirement Accounts (IRA). Regarding the applicability of khums in this process, the same rulings apply as in the 401(k) except there are no employer contributions to the savings.

Leave a Comment:

You must be logged in to post a comment.